Contents

Key Takewaways

- Cash flow refers to the money that enters and leaves a business

- A cash flow statement tracks a company’s cash inflows and outflows over a set period. This is a standard financial statement that is generally mandatory, like the balance sheet and the income statement.

- To prevent cash flow problems, monthly cash flow audits and cash flow forecasts are useful tools

- To ensure positive cash flow, you may take steps to lower overhead costs, increase profit margins, and prevent delayed customer payments

It seems counterintuitive, but even a highly profitable business can fail because it doesn’t have enough cash to keep itself running. In fact, flawed cash flow mismanagement is one of the biggest reasons that some businesses fail in their first year. A successful business is one that keeps a close eye on even the pennies that come and go; this is no easy task, so this article is here to make it a little more doable.

Cash Flow Definition

Cash flows are the money that goes in and out of a business. Money can come in from operations (or sales), investments, and financing, and money goes out to cover expenses.

Positive cash flow means that a company has enough liquid assets to cover expenses, pay dividends to shareholders, and reinvest money into the business. Therefore, looking at a company’s inflows and outflows is how we assess a company’s liquidity and financial performance.

As mentioned before, even profitable companies can be short on working capital. For example, a company delivers a service to their customers but lets them pay one year later. The company treats the sale as revenue, but it will not receive the payment until next year. All the same, operating costs still need to be paid each month. In this way, even a business that is making a profit on paper can lack sufficient cash for daily operations.

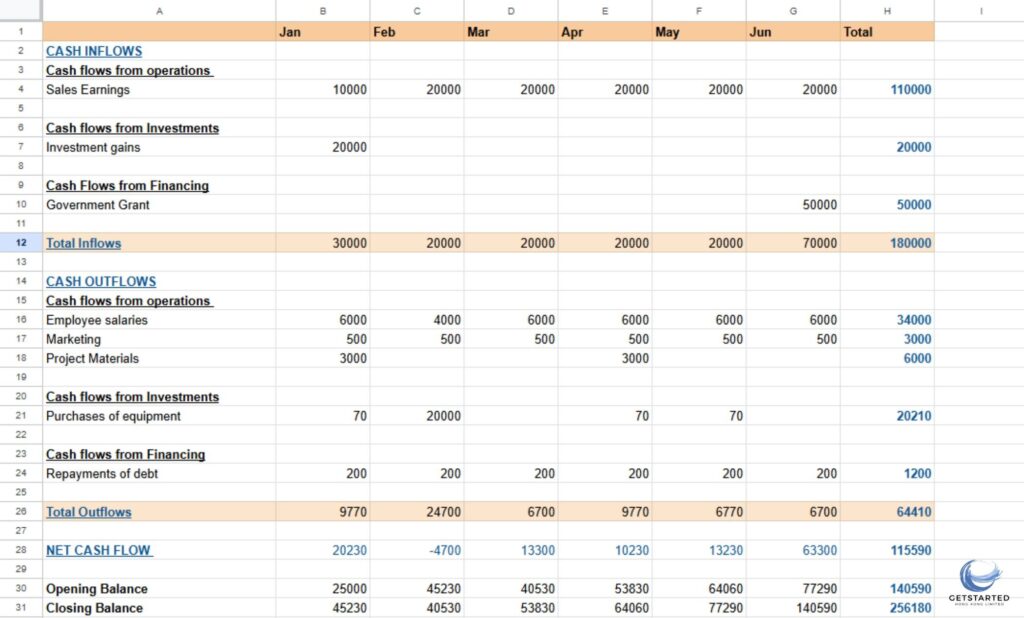

What is a cashflow statement?

The best way to analyse a company’s liquidity is by preparing a cash flow statement (CFS). This statement tracks a company’s cash outflows and inflows over a specified period. The preparation and filing of this financial statement, much like the balance sheet and the income statement, is a reporting requirement in most jurisdictions.

Components of a cash flow statement

There are 3 main sections in a CFS. These are:

- Operations, reporting cash inflows and outflows from main business activities, such as salary payments, purchasing supplies, and selling inventory.

- Investing, dealing with investment gains and losses, including money spent on property and securities.

- Financing, providing insights on the flow of money between the company and its owners and creditors. The source of the cash is usually equity of debt, like selling stocks and bank loans.

The sum of the funds generated by these 3 sources is called net cash flow.

How To Keep Track of Cashflow

Frequent cash flow audits

By closely monitoring your cash on a weekly, monthly, or quarterly basis, you’d have a better chance of detecting outliers and issues before they turn into shortages in working capital.

There are multiple accounting SaaS solutions online offering tools for cash management. These include Xero, Quickbooks, and Sage. With the aid of automatically generated reports and robust cash flow analysis tools, you’ll be able to make data-driven decisions on where to reinvest surplus cash, where to cut costs, and more.

Cash Flow Forecasts

A cash flow forecast would also help you detect potential problems before they rear their heads. You may do the following to project your cash flow:

- Analysing market trends: look into other businesses in your industry and consider their sales growth, and how they’re faring amidst changing market trends. This will help you anticipate changes in your own revenue and expenditure

- Analysing past data: find patterns, trends, and identify fluctuations in your past CFSs to get a better sense of where your cash will go in the coming months

Preventing Cash Flow Problems

The work of maintaining a healthy cash flow is more than just generating forecasts and reports every once in a while. Indeed, the following steps are part and parcel to the daily operations of your business.

1. Assess Profit Margins

Low working capital is often the result of tight profit margins. Look for ways to streamline your operations, and the possibility of renegotiating supplier contracts. Also ask the question, how much can you raise prices before you drive your customers to your competitors? This will help you get a better sense of the effectiveness of your pricing strategy.

Strengthen payment collection procedures

If your customers have a tendency to pay you long after you’ve delivered your products or services, this can destabilise the flow of funds into your company. You may consider requiring deposits for large deals and setting clear payment terms with your customers upfront. An invoice automation software that can send automatic payment reminders to your customers can also gently nudge your customers to pay you in a timely manner.

Minimize Overhead Costs

Expenses like office rent, employee salary payments, and utilities must be paid regardless of how much your business makes, and these costs can quickly add up and put a strain on your finances. This is especially true for startups without a stable stream of revenue.

For newer businesses, consider cutting out non-essential costs. For example, instead of hiring full-time staff, consider outsourcing labour. Instead of renting an office, consider utilising coworking spaces or virtual offices.

Properly Timing Payment Schedules

You might consider reopening negotiations with suppliers to get extended payment terms. This is also a good opportunity to check for possibilities of preferential pricing and volume discounts.

Building a Cash Buffer for Daily Operations

Most businesses are vulnerable to seasonal sales dips, unexpected expenses, and economic downturns. To protect your business from these common disruptions, it would be wise to build up a reserve of cash that is large enough to cover 3 to 6 months of operating expenses.

A business faces multiple challenges every single day, but if you take these steps, there is no reason you cannot anticipate and quash liquidity problems before they even arise.

Frequently Asked Questions about collection of personal data

1. What is tracking cash flow?

Tracking cash flow is the practice of recording and calculating the cash that flows into and out of a business over a set period of time. This can be done through preparing a financial statement called the cash flow statement. The cash flow statement records cash flowing in and out from the company’s operations, investment activities, and financing activities, showing a business’s ability to fulfil its financial obligations.

Cash inflow is the money that enters a business through multiple sources. These can be payments from customers for goods and services provided, investments, or bank loans. On a financial statement, the sum of all the money that flows into a business is referred to as “net cash flow.”

3. What is the best way to track cash flow?

The best ways to track cash flow include doing cash flow audits frequently. Some businesses opt to do so on a monthly basis, and others even on a weekly basis. Another method of tracking cash flow is to make cash flow forecasts. This involves analysing your past cash flow statements and market trends. Both of these steps would help you detect cash shortages before they snowball, and to make decisions about where to increase funding and cut costs based on real data.

4. What are five rules of cash flow?

There are five things that business owners can do to ensure positive net cash flow. These are:

- Raising profit margins

- Minimizing the gap between the delivery of goods and services and the collection of customer payments

- Minimizing ongoing overhead costs

- Building a cash reserve for daily operations, and

- Negotiating for extended payment terms with suppliers